May Market Update

The market continues to show remarkable consistency, with most key metrics looking very similar to this time last year. Average sales prices increased 1.2% year-over-year, driven largely by strength in the detached single-family home market, where prices rose 3.2%. Meanwhile, condos and townhomes continue to face softer demand, creating a noticeable divide between attached and detached housing segments.

One of the more notable shifts this month is a decline in new listings, which fell nearly 10% year-over-year. While overall inventory remains relatively stable, fewer homeowners appear willing to enter the market as higher interest rates make moving more challenging. This could mean less competition for sellers, while also limiting the additional inventory some buyers have been waiting for.

Beyond those changes, many market indicators—including pending sales, closed sales, days on market, showing activity, and months of supply—remain largely unchanged from last year. The data continues to reinforce a market that is neither accelerating nor declining significantly, but instead operating at a steady pace.

For buyers, the biggest opportunities remain at both ends of the spectrum: being competitive on desirable new listings or negotiating on homes that have been sitting longer than expected. For sellers, pricing remains critical. While well-positioned homes are still selling close to asking price, properties that linger on the market often require price adjustments to attract activity. Overall, this remains a market that rewards realistic expectations, strong local knowledge, and a willingness to adapt to current conditions rather than waiting for dramatic changes.

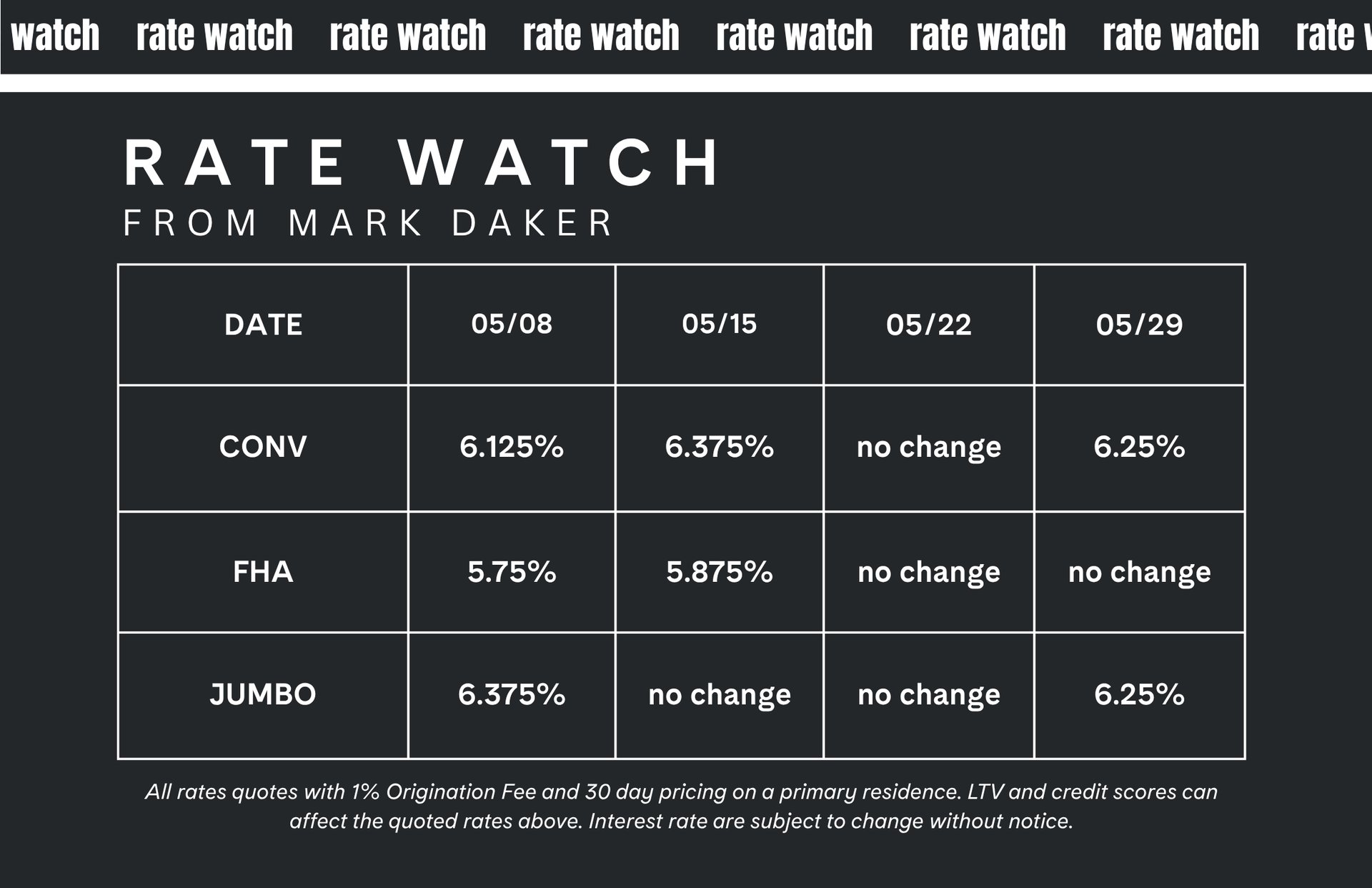

Mark Daker for Ameris Bank Insights

May brought continued volatility to mortgage rates, though much of the movement remained driven by geopolitical developments rather than traditional economic indicators. Ongoing conflict involving Iran continued to create uncertainty in financial markets, with mortgage rates responding to shifting expectations around inflation, energy prices, and the potential for a broader economic impact. While hopes for a resolution periodically helped rates move lower, delays in peace negotiations often pushed rates back upward.

Economic data released throughout the month largely met expectations. Inflation readings, employment reports, and GDP figures all pointed to a relatively stable economy, while stronger-than-expected job creation reinforced the resilience of the labor market. At the same time, the strength of the economy reduced expectations for near-term Federal Reserve rate cuts, with some market participants even beginning to anticipate the possibility of future rate hikes if inflationary pressures persist.

Toward the end of the month, signs of progress in international negotiations helped calm markets and allowed mortgage rates to ease somewhat from their recent highs. Despite occasional improvements, May highlighted the continued influence of global events on mortgage rates, with market sentiment and geopolitical headlines often outweighing the impact of routine economic reports.