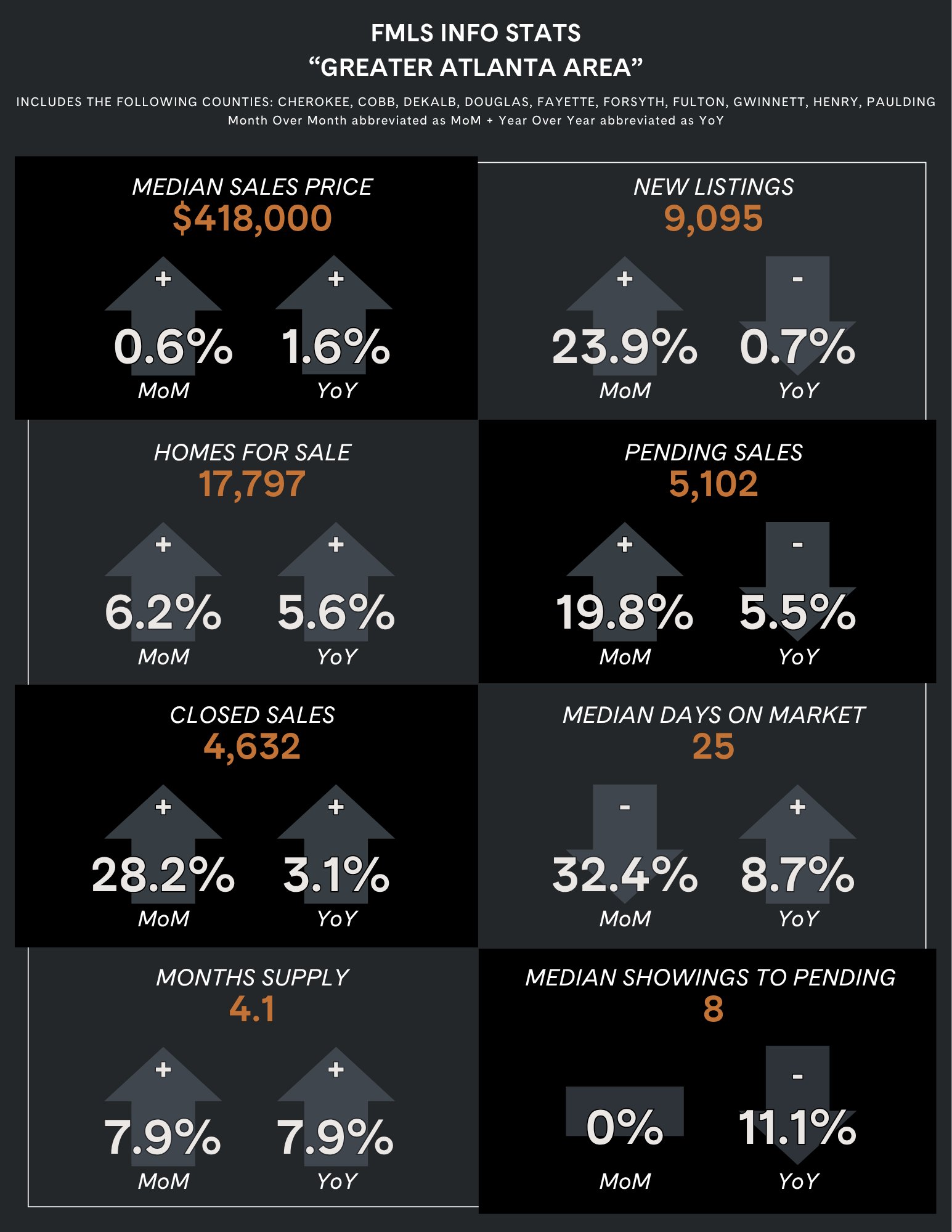

March Market Overview

The real estate market is showing mixed activity depending on property type, price point, and location. March closed sales were slightly up year-over-year, largely driven by stronger pending activity in late February when interest rates dipped. However, pricing trends are inconsistent—condos and townhomes saw declines, while single-family homes experienced modest appreciation, highlighting the importance of analyzing the market at a more granular level.

Market conditions also vary widely across segments. The luxury market is notably active, with increased sales volume and buyers who are often less sensitive to price and more focused on securing the right property. In contrast, entry-level and condo markets are facing more resistance due to affordability challenges, higher inventory, and stricter lending conditions. Overall inventory and transaction volume remain similar to last year, but many agents report that deals are taking more effort to get across the finish line.

A growing factor influencing client behavior is the use of AI tools to estimate property values and market conditions. While these tools can provide a starting point, they are highly dependent on the inputs provided and often fail to account for intangible factors like location quality, property uniqueness, and buyer demand. This can lead to misleading conclusions, reinforcing the need for agent expertise to interpret data and guide clients effectively.

For buyers, hesitation remains a key challenge. Many are waiting for the “right time,” but agents are finding success by reframing the conversation around long-term goals, financial stability, and the reality that perfect market timing is unlikely. For sellers, outdated expectations from previous market highs are still common, requiring a combination of data, patience, and market exposure to align pricing with current conditions. Investors, in particular, are proceeding cautiously, as higher interest rates and softer rental conditions make it more difficult to achieve clear returns without well-defined criteria.

Overall, while the market has lost some momentum due to rising rates and broader economic uncertainty, it has not stalled. Activity levels remain steady, but with more cautious participants and greater variability across segments, making hyper-local knowledge and clear client guidance more critical than ever.

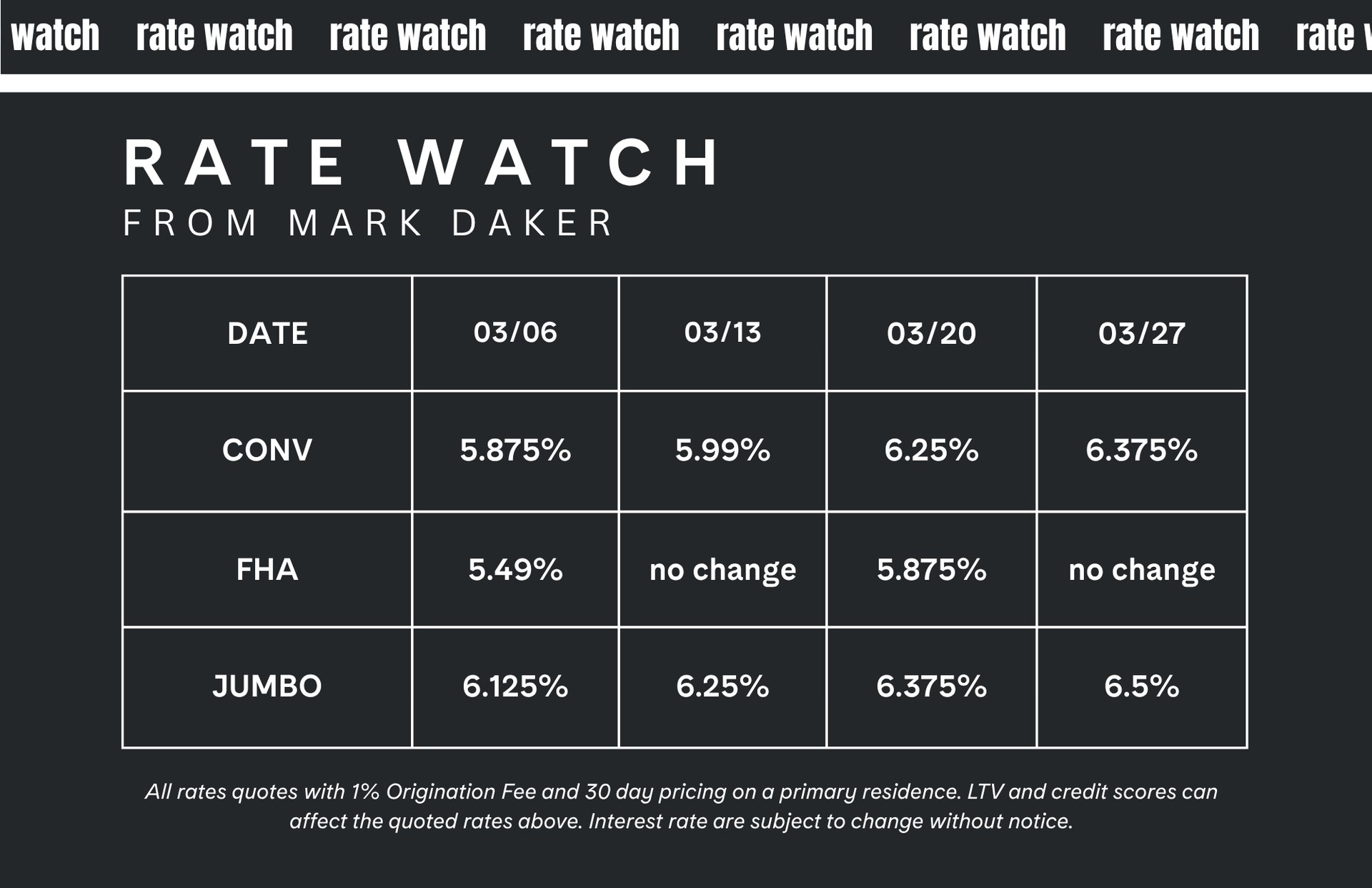

Mark Daker from Ameris Bank Insights

Mortgage rates shifted sharply in March, reversing February’s decline and bringing renewed volatility to the market. Geopolitical tensions, particularly the conflict involving Iran, pushed oil prices higher and increased inflation concerns, prompting markets to quickly adjust expectations for Federal Reserve policy. As a result, mortgage rates rose by roughly half a percentage point in just a few weeks, moving from multi-year lows to near nine-month highs.

This marks the fastest rate increase since the post-pandemic adjustment period and highlights how quickly external events can reshape the outlook. Despite the movement, broader economic indicators such as employment and housing activity have remained relatively steady, and mortgage applications continue to trend higher year over year.

Much of the recent volatility is tied to global developments rather than underlying economic weakness, leaving room for potential improvement if conditions stabilize. For now, rates remain sensitive to ongoing uncertainty.