January Overview

January in the Atlanta real estate market was widely described as “slow,” “indecisive,” and “frustrating,” though not universally negative. Many agents reported buyers and sellers sitting on the fence, hesitant to make decisions after months of rate volatility and market shifts. Buyers in particular are overanalyzing price and timing, often waiting to see if activity materializes before submitting offers. However, some agents are finding success by taking a more proactive, “hand-holding” approach, hosting exploratory showings, drafting practice offers, and breaking the process into smaller steps to help clients move past fear and inertia. While overall transaction volume was down year over year, there is optimism that improving affordability (slightly lower rates, flat pricing, and wage growth) could bring more buyers back into the market.

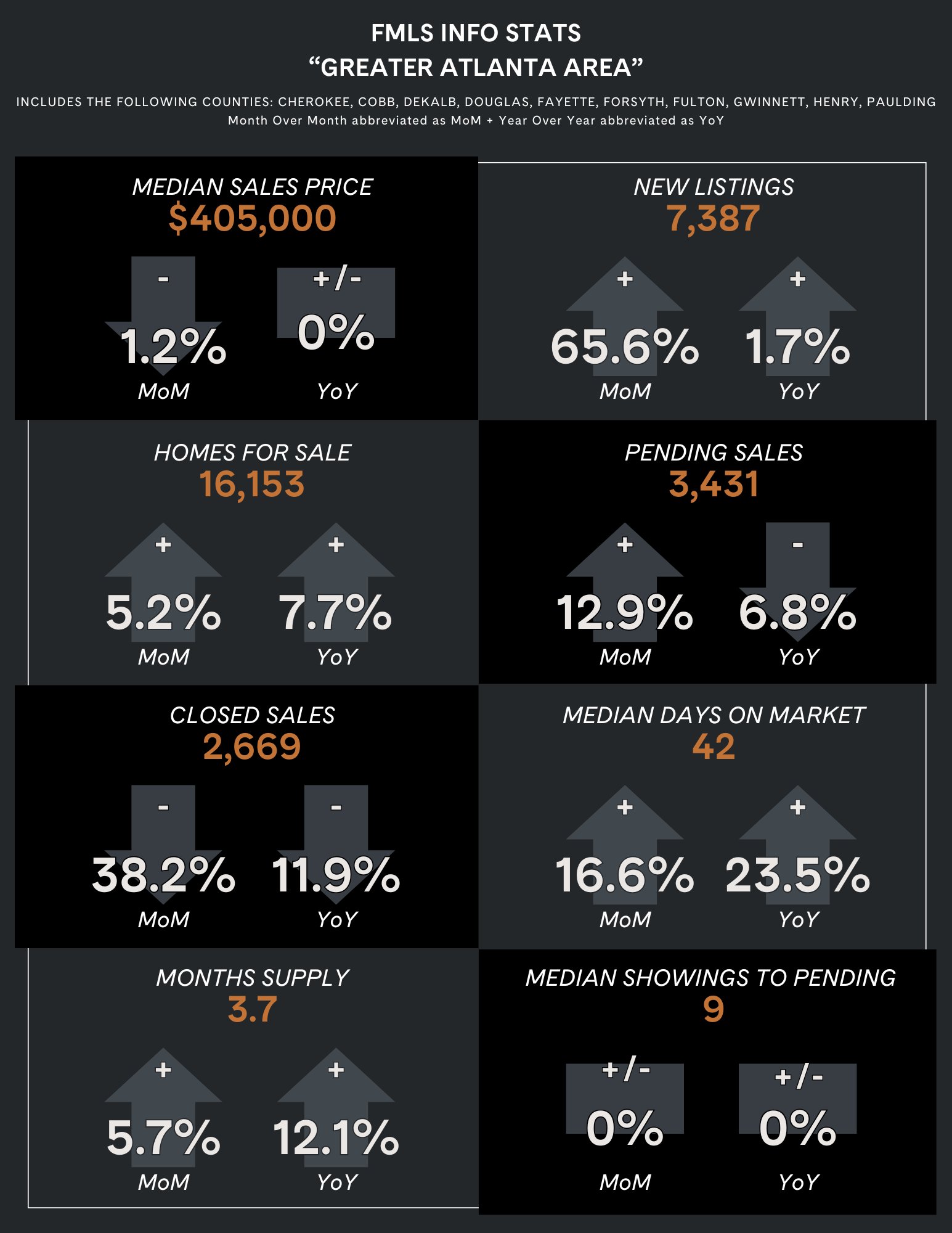

From a data standpoint, prices and new listings in Greater Atlanta are nearly flat compared to last January, signaling stability rather than a market decline. However, total inventory is up modestly, pending and closed sales are down, and the average days on market has risen to 60 days (with condos averaging significantly higher). This longer timeline requires agents to reset seller expectations and over-communicate consistently. Many emphasized the importance of weekly updates, sharing hyperlocal data, and reminding sellers of broader market conditions to combat frustration. The consensus: if the market is similar to last year, agents must adjust their strategies and increase effort to generate different results.

Pricing strategy emerged as a key theme, particularly around meaningful price reductions. Data shared in the meeting suggested that price drops under 4% tend to have little impact, while reductions of 4% or more produce noticeably better results. Incremental cuts of $5,000–$10,000 are often ineffective, especially in higher price points, and can lead to stagnation. On the buyer side, agents are seeing—and successfully negotiating—offers 10% or more below list price, particularly on homes sitting 100+ days. The overall takeaway: negotiation is back, patience is required, and success in this market depends on strategic pricing, creative problem-solving, and consistent communication.

Mark Daker from Ameris Bank

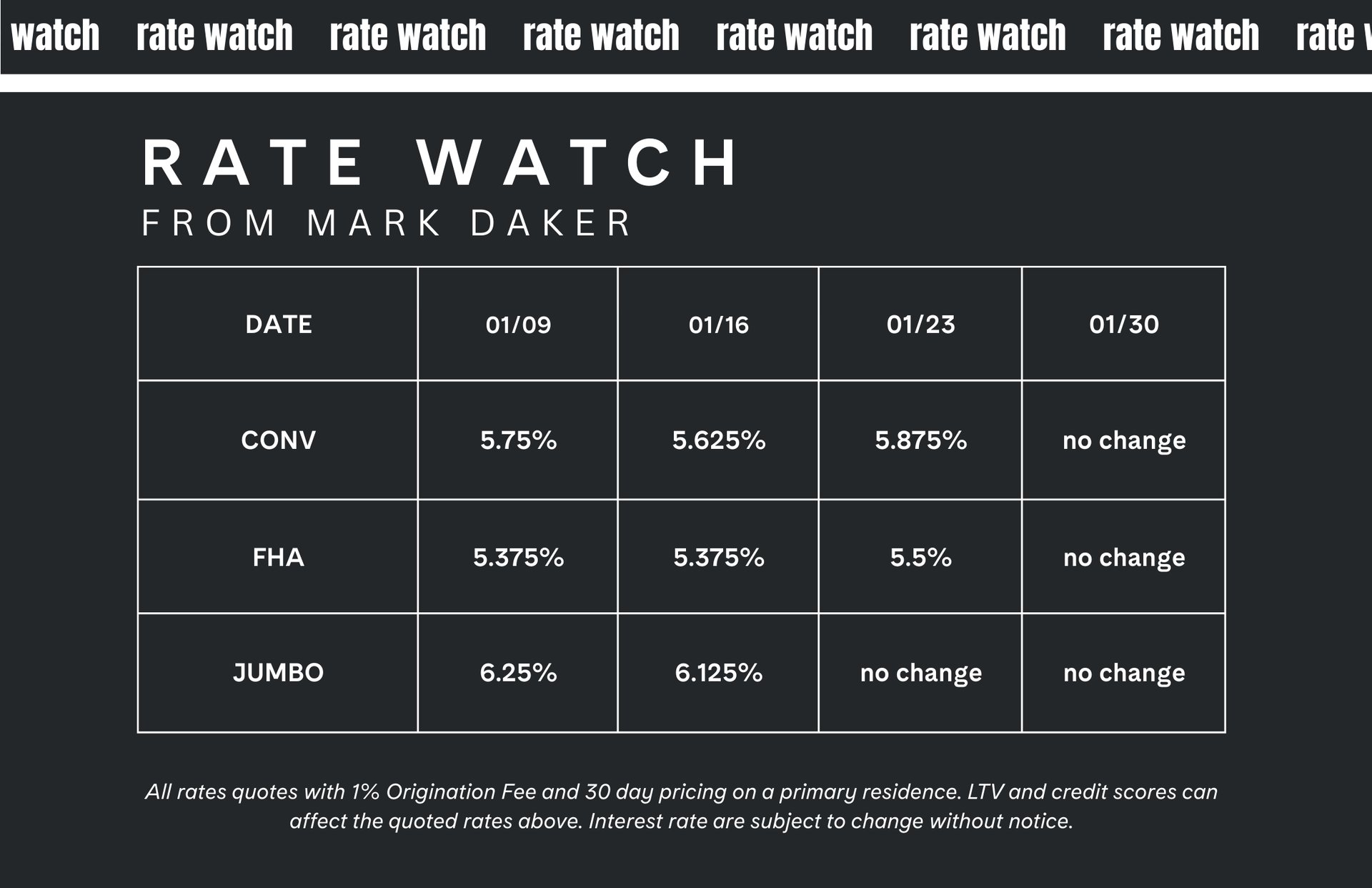

Mortgage markets saw a wave of headlines this week, driven largely by updated labor data and Fed developments. While job creation in 2025 has slowed compared to prior years, the unemployment rate held steady, and markets reacted calmly as much of the news was already anticipated. Stocks rallied again on expectations that employment stability could support growth, and mortgage rates remained virtually unchanged overall.

Rates briefly touched multi-year lows early in the week before giving back some gains, though they still ended near their lowest levels in quite some time. Ongoing discussion around a proposed $200 billion mortgage bond purchase plan has helped fuel optimism for lower rates, even though no funds have yet been deployed. Other economic data was generally rate-friendly, including slightly lower inflation readings, improved jobless claims, and modest strength in retail sales and manufacturing. The Fed left rates unchanged, as expected, and commentary offered little surprise. Overall, steady inflation and a resilient job market continue to support the potential for improved rate conditions as we move further into 2026.