April Market Update

The market continues to feel active, steady, and very much in line with a typical spring season, but one of the biggest themes right now is how hyper-local everything has become. Broad market generalizations are becoming less useful, as conditions can vary dramatically from one neighborhood—or even one street—to the next. Pricing trends also continue to split by property type, with average sales prices up 3.7% year-over-year overall. Detached single-family homes saw stronger appreciation, while attached properties like condos and townhomes experienced slight declines, reflecting differences in buyer demand.

Move-in-ready homes remain highly competitive, while properties needing updates are facing more resistance from buyers. At the same time, many homes that struggled to sell during the slower winter months are finding success after returning to the market this spring. Although conversations around interest rates, economic uncertainty, and global events continue, the overall market data remains surprisingly stable. Rates increased in April, yet pricing still moved upward, reinforcing that the market is not shifting dramatically in either direction.

For buyers, opportunities are beginning to emerge on homes that have been sitting for more than a few weekends, creating more room for negotiation than many consumers realize. While aggressively low offers may not make sense on fresh listings with strong activity, there is more flexibility on homes that have lingered on the market. Overall, the market remains balanced and resilient, but success is requiring more strategy, realistic expectations, and a strong understanding of local market conditions.

Mark Daker from Ameris Bank Insights

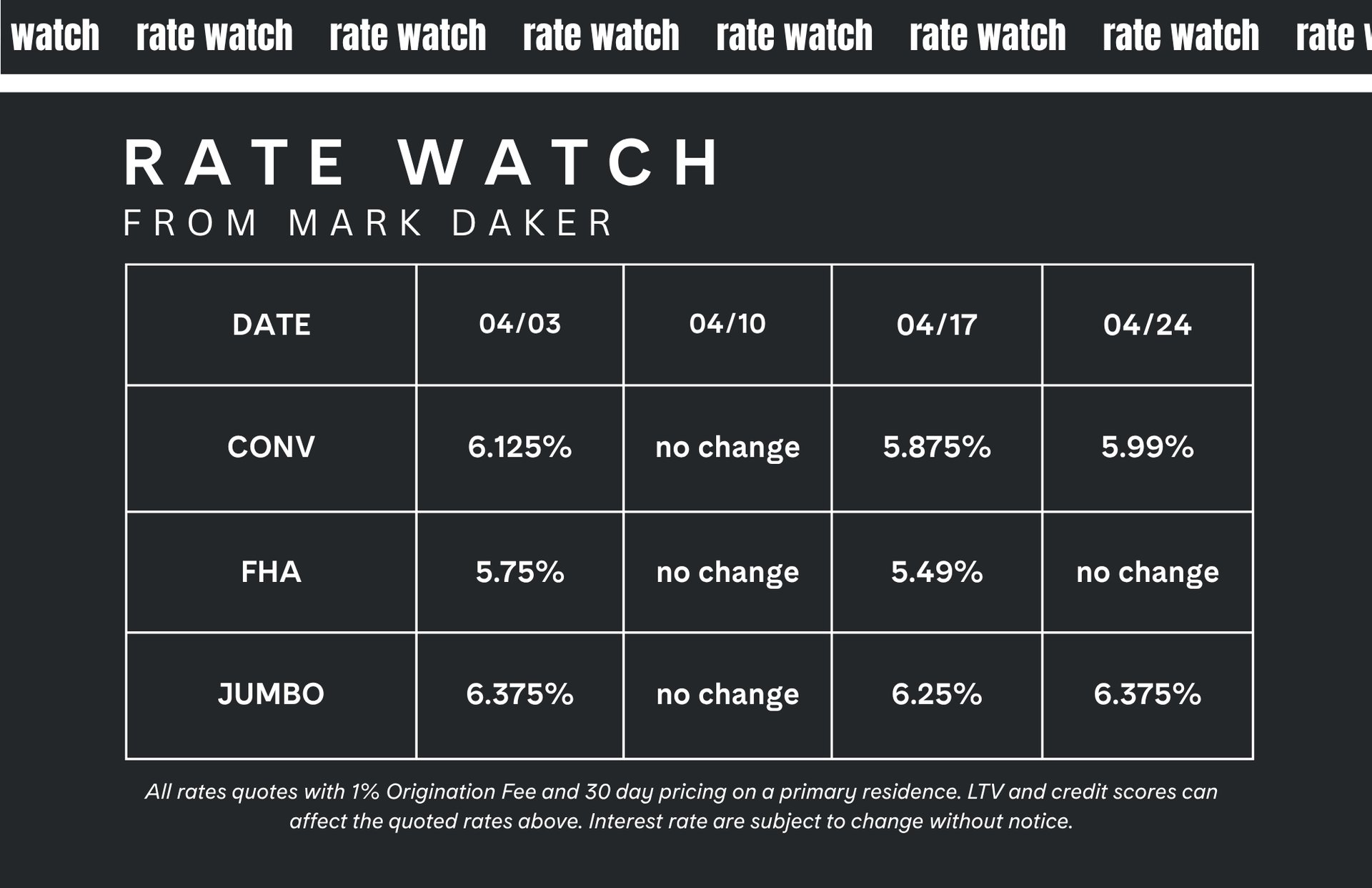

April brought continued volatility to mortgage rates, though the sharp swings seen in March began to moderate as markets adjusted to ongoing geopolitical developments. Much of the month’s movement remained tied to the conflict involving Iran, with mortgage rates reacting quickly to shifts in oil prices and broader market sentiment. Temporary signs of easing tensions helped rates move lower at several points throughout the month, while renewed uncertainty continued to create fluctuations.

Inflation data released during April showed persistent pressure across several sectors, largely driven by elevated energy costs. Markets appeared to have already priced in much of the expected inflation impact. At the same time, economic data remained relatively resilient, with stronger-than-expected employment figures reinforcing the view that the broader economy continues to hold steady despite global instability.

Toward the end of the month, a ceasefire overseas and improving global oil flow helped calm financial markets, pushing mortgage rates to some of their lowest levels in weeks. Overall, April reinforced how heavily mortgage rates remain tied to geopolitical developments, with markets continuing to respond more to global headlines than traditional economic indicators.